Same Drinkers. Fewer Nights.

Why frequency compression is a harder problem than participation decline

There’s a version of this night you recognize. Out the door without overthinking it. One drink turning into two. Running into someone you didn’t expect to see. It’s still there, somewhere. Just harder to reach. You run through it, do the quick math, and stay put.

A night went missing. Not symbolically. Functionally. And it didn’t just happen to you.

Gallup has the headline everyone’s seen: participation down from 67% to 54% between 2022 and 2025, the lowest reading since they started tracking in 1939.

That’s been read as a recruitment problem. Fewer drinkers, weaker funnel. Just wait for the cycle to turn. Some of that is real. Younger consumers are entering later.

But the change runs through the base. Same people. Fewer nights.

In Gallup’s latest survey, active drinkers reported 2.8 drinks in the past week, down from 3.8 the year before. That’s the lowest level since 1996.

It takes a lot to move an average that held steady for decades. Losing one night a week will do it. Something that used to happen without planning, now happening less often or not at all.

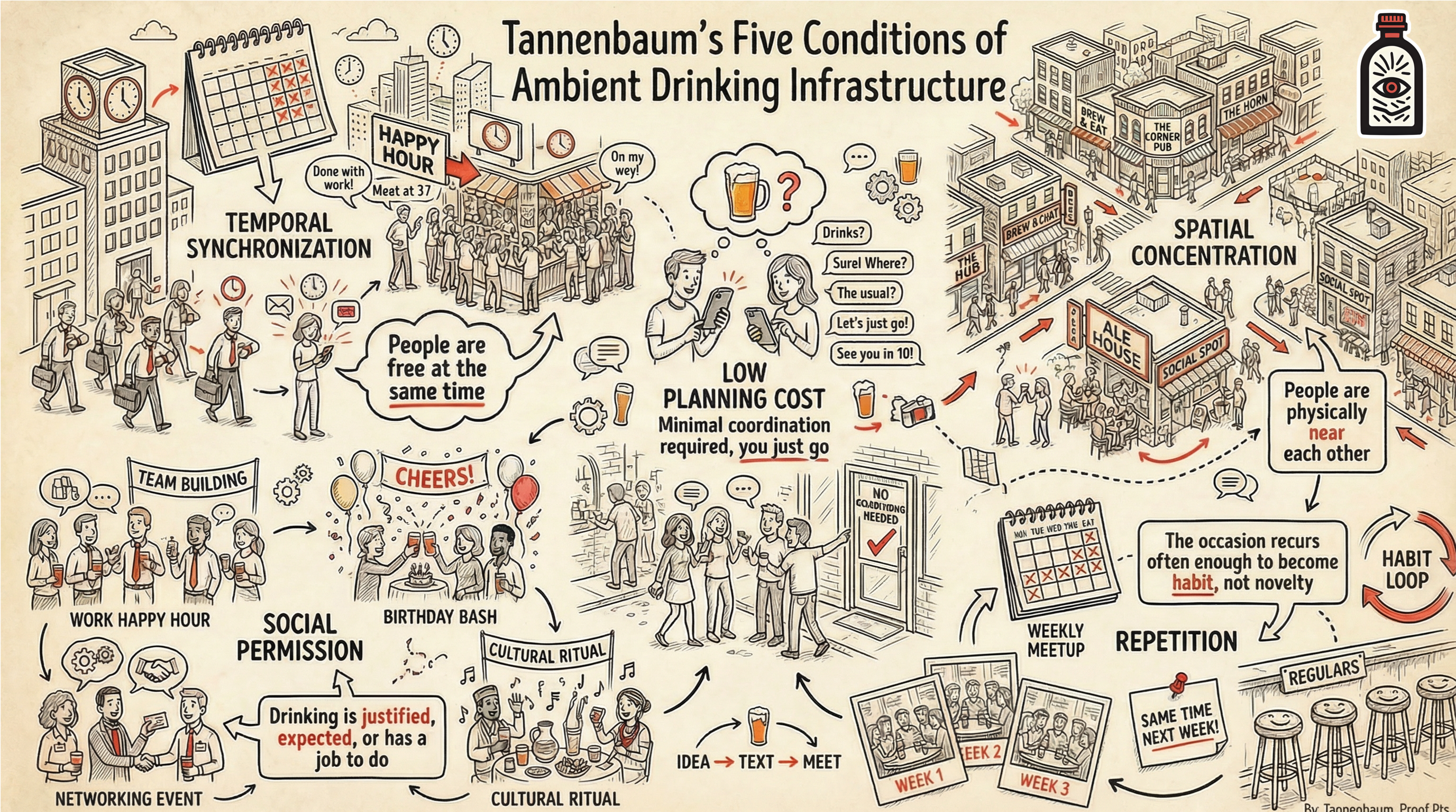

That occasion didn't disappear purely because people decided to drink less. It disappeared because the structural conditions that made it automatic stopped being available. A drink has never existed in isolation. It exists inside an occasion, a dinner, a happy hour, a game, and occasions have requirements.

People need to be free at the same time, near each other, near a location, with low enough friction that nobody has to plan it. Even drinking along requires some level of cultural permission. For most of the twentieth century, daily life quietly met those requirements. Now it doesn't as reliably, and the casual moment is the first casualty.

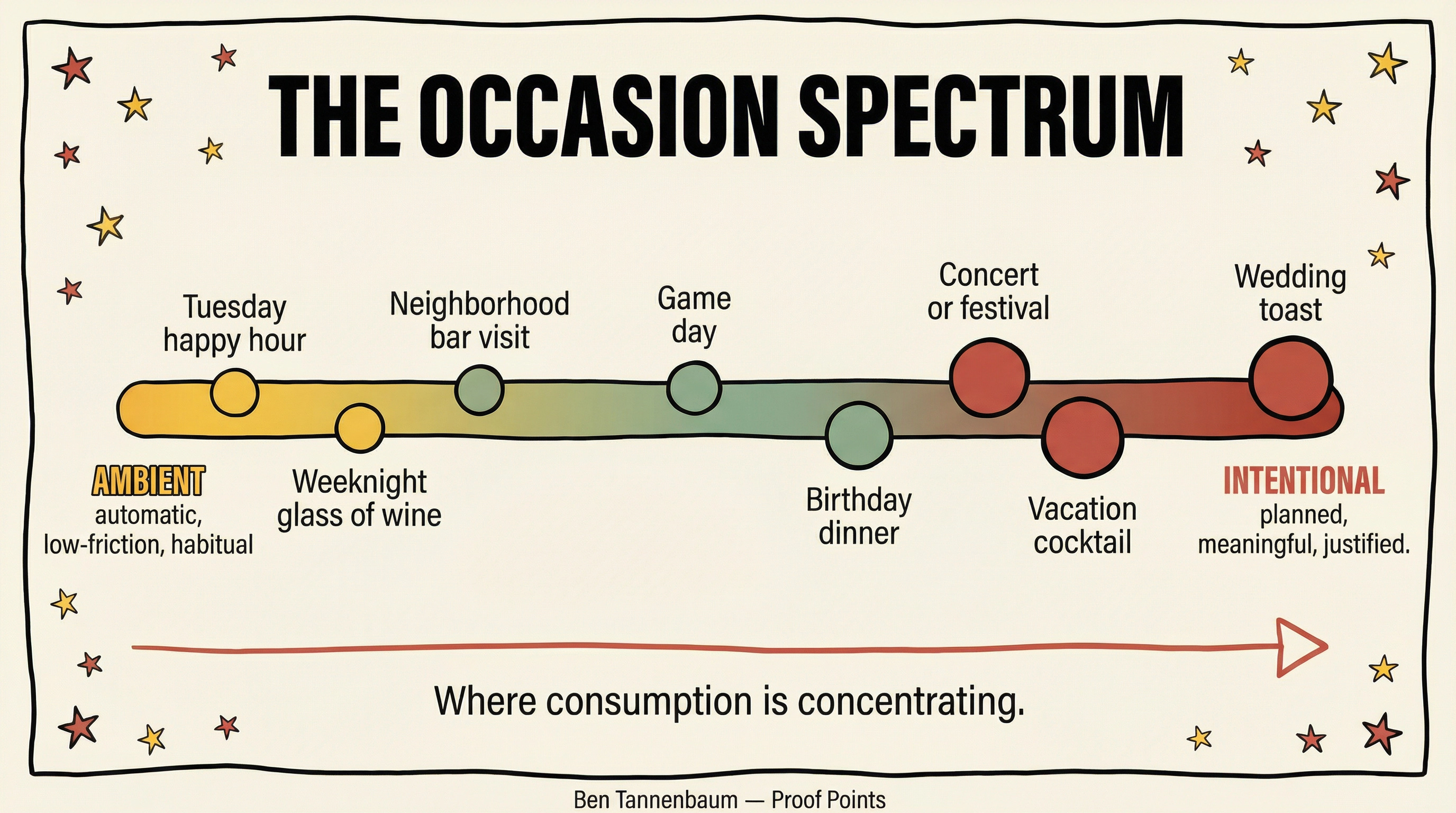

The occasions holding are the ones that carry their own structural weight. Events, travel, celebrations, premium dining where drinking is architecturally embedded. The ones eroding are the ones that used to happen without anyone deciding they should.

When the casual Tuesday dinner becomes a considered expense rather than an automatic behavior, the drink that accompanied it becomes a considered expense too. The occasion migrates from ambient to planned. And planned occasions happen less often.

This is what frequency compression looks like from the inside. The machine still runs. It just fires less often.

Case in point: Citi upgraded Constellation to Buy this week. The thesis: easy comps, a recovering Hispanic consumer base, and World Cup activation in June. RBC made the same call with the same logic. Neither analyst is arguing that the category has structurally recovered. Both explicitly flag that Constellation's margin targets are coming down as the price of returning to volume. That is not a recovery story. That is one portfolio executing better inside a flat system, at lower profitability than before. The frequency story hasn't changed.

I wrote in February about why the stabilization narrative was premature.

The response raised a consistent follow-up: if the diagnosis is frequency compression, what do you actually do about it?

So here’s the strategy piece.

What This Means for Brand Strategy

Distribution density over diffuse awareness

As occasions concentrate into fewer channels and moments, physical availability in those specific contexts becomes more valuable relative to broad awareness. A brand that owns the festival cooler or the premium back bar can capture more profit dollars than a better-known brand that simply isn’t there. This is a re-weighting, not a rejection of brand building. Mental availability still matters, but its value increasingly depends on whether it converts in the specific moments that remain.

Occasion engineering as a core discipline

For most of the premiumization era, marketing's job was to move consumers up the ladder inside occasions that already existed. If occasions are contracting, the job shifts. Brands and venues that can create or intensify the structural conditions of existing occasions hold the growth leverage. White Claw made this explicit this month. Their research shows 72% of groups default to beer, but 80% would switch if prompted. That gap between default behavior and actual preference is the entire strategic opportunity right now. White Claw is not positioning against beer's liquid. They are positioning against beer's inertia. That reframe, from product competition to habit disruption, is where the leverage has moved, and it applies well beyond the seltzer category. The brands that understand they are competing against autopilot, not against each other, are playing the right game.

RTDs as ecosystem anchors

Ready-to-drink formats solve friction problems that traditional spirits formats struggle with: portability, simplicity, low commitment. For a consumer who now treats the casual drinking occasion as optional rather than automatic, those properties matter. The strategic value of RTDs is less about category growth and more about keeping a consumer inside the brand ecosystem during the long stretches between intentional occasions. RTDs are share gainers right now, not category expanders. The formats that make casual drinking easier are growing. The occasions themselves are not.

SKU rationalization accelerates

Fewer occasions means fewer need-states to serve. The long tail of product assortment becomes harder to justify when the shelf is competing for a smaller number of purchase moments. The exception: SKUs that own a very specific, high-value occasion, the spicy margarita mix at the backyard cookout, the barrel-aged stout at the craft bar, can survive if the occasion is defensible. What loses is everything in between: broadly available, occasion-agnostic SKUs competing for ambient moments that are disappearing.

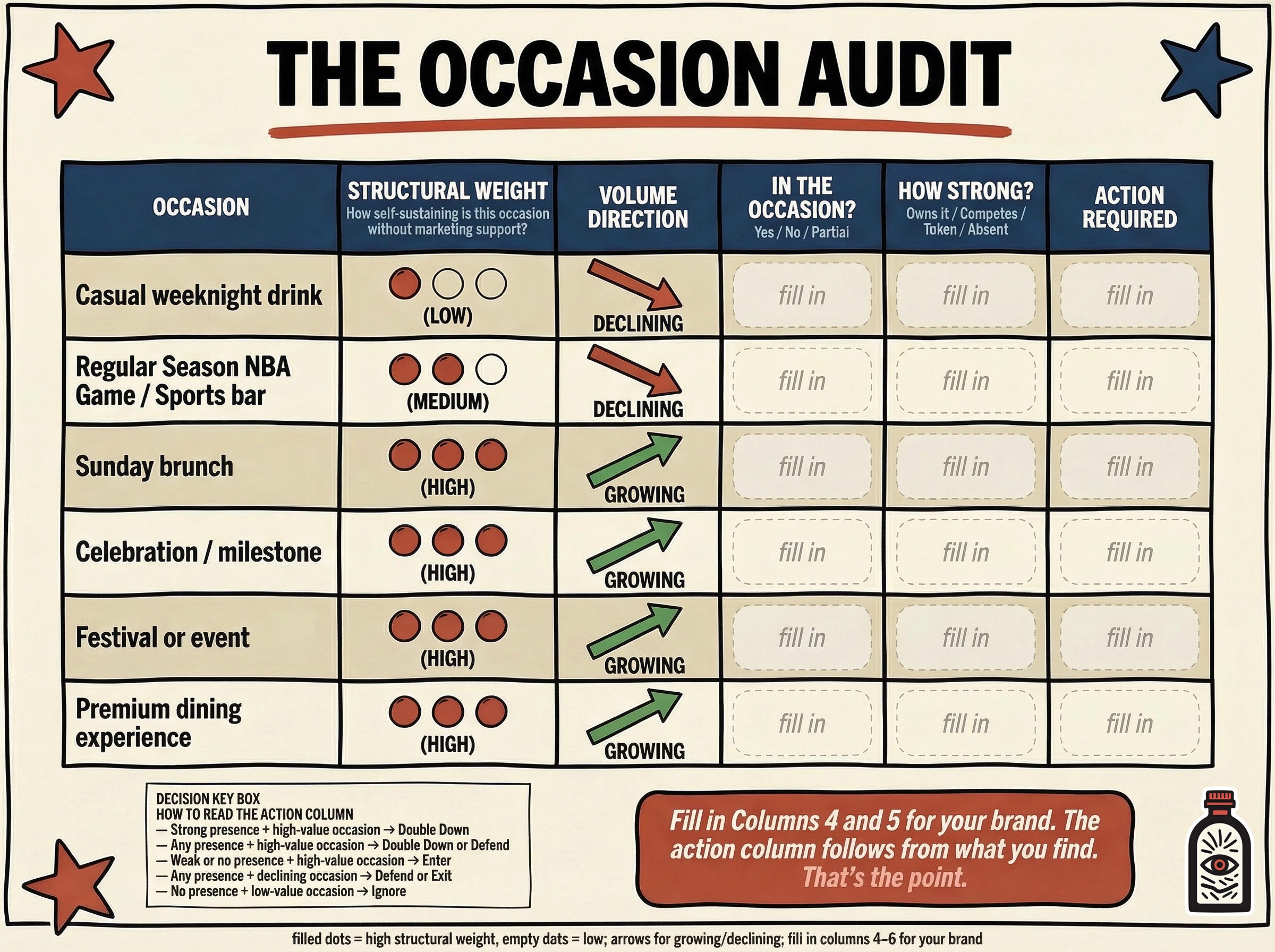

The Occasion Audit below maps six of the occasions relevant to the frequency compression argument, but they represent a fraction of the full landscape brands should be mapping. Fill in the last two columns for your brand. The action column is what informs your strategy.

From Margin to Occasion Coverage

For most of the last decade, the key financial story in spirits was margin expansion. Mix improved, price tiers climbed, profitability strengthened. That focus made sense when the base of occasions was stable.

When the strategic challenge becomes occasion coverage, a different metric begins to matter. Occasion coverage, in this context, is the absolute profit dollars a brand generates across the full map of occasions where drinking still happens. How many of those remaining moments it shows up in, and how profitably. A brand with slightly lower gross margin but strong presence in airport bars, sports events, and high-energy casual dining may generate more total profit than a leaner brand that dominates only one upscale channel.

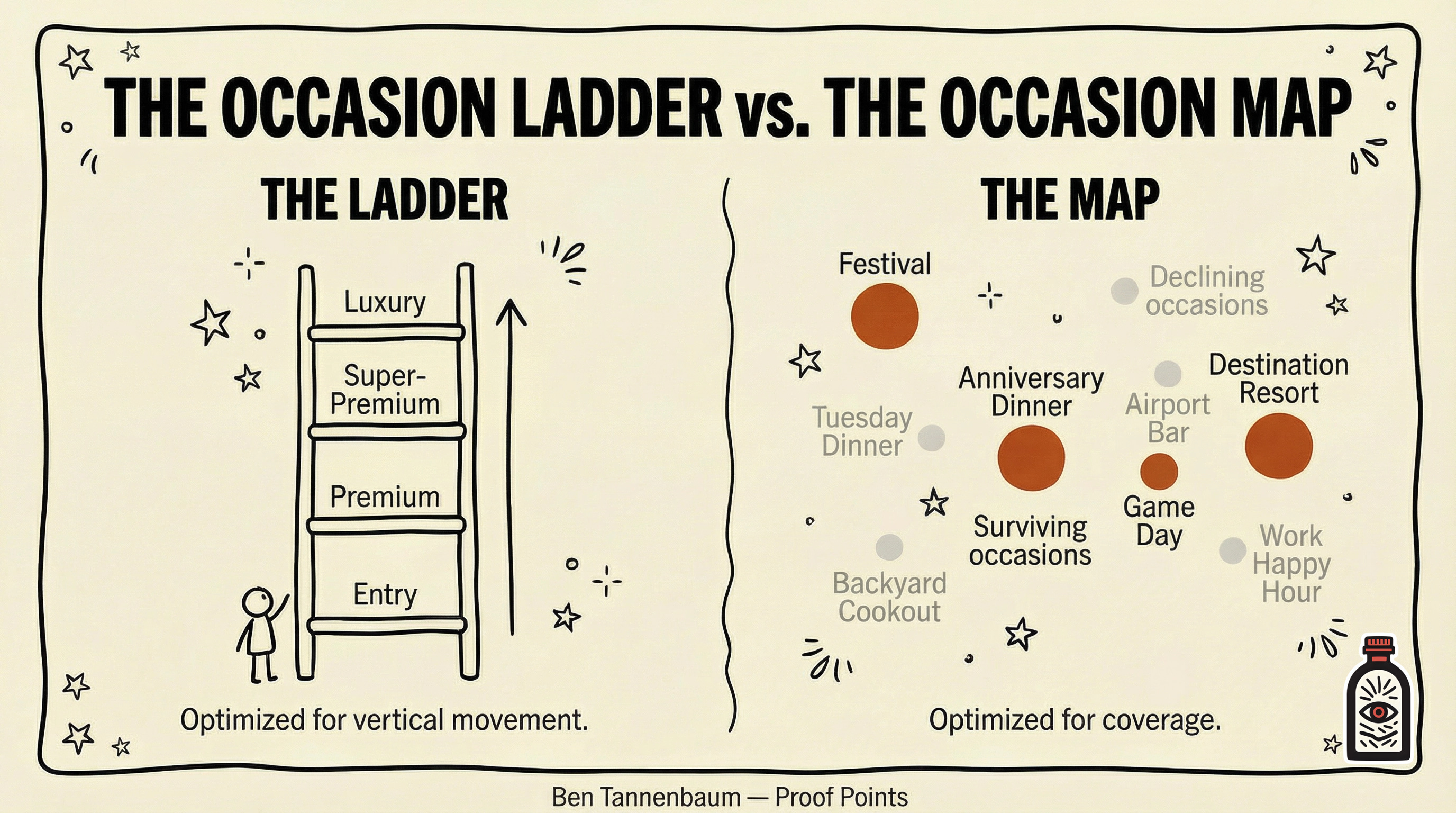

Margin optimization inside a contracting occasion base is a strategy for managed decline. Occasion coverage is the strategy for growth. The ladder tells you where to climb. The map tells you where to show up. Right now, the map is the better tool.

The Signal to Watch

A structural thesis requires ongoing validation. St. Patrick's Day 2026 is the cleanest recent confirmation. BeerBoard tracked draft beer volumes up 4% across the total holiday period compared to 2025. Draft revenues fell 4% over the same period. More people drank more beer on the industry's highest-intent beer holiday and the industry made less money doing it. BeerBoard attributed the spread to a shift from craft and imports toward domestic lager, accelerated by deals and specials. That is not a recovery signal. That is volume without value, which is a different problem than volume decline, and in some ways a harder one.

The data through 2025 supported the structural read. We're three months into 2026 and nothing has changed that. The World Cup window and the summer holiday stack will be occasions with a story attached and the numbers will look fine. Everyone will be watching those. Watch the Tuesdays in between. Either people go out or they don't. Right now they mostly don't.