The Illusion of Stabilization

Why easier comps aren't the same thing as healing

The tone is shifting. You can feel it in the earnings previews, the analyst notes, the careful optimism creeping back into distributor commentary. Executives are finding phrases like “pockets of strength” and “sequential improvement.” After two years of volume contraction, the beverage alcohol industry is ready to believe the worst is behind it.

Then Diageo reported earnings this week. CEO Dave Lewis told analysts the company is underrepresented in the mass market, signaled it may selectively cut price, and acknowledged margins could compress. That isn’t a tweak. The Sir Ivan Menezes era at Diageo optimized hard for mix. Premiums up, volume secondary, margins protected. Lewis is flagging that the trade-off no longer works. The largest spirits company in the world just said the premiumization engine needs to be rethought.

I’d love to call that a recovery signal, but it reads more like confirmation.

What the industry is calling stabilization may be something else entirely: the natural arithmetic of a system that’s finished shrinking, not one that’s started healing.

Stabilization in a shipment report doesn’t necessarily mean stabilization in people’s lives. Adult drinking participation is still well below pre-pandemic levels. Casual weeknight bar traffic hasn’t returned to its old baseline. Many of the rituals that used to generate default consumption - after-work drinks, neighborhood drop-ins, loosely planned gatherings - remain thinner than they were five years ago. The math may be stabilizing. The culture hasn’t.

The Denominator Problem

Let’s start with the math, because its doing most of the heavy lifting right now.

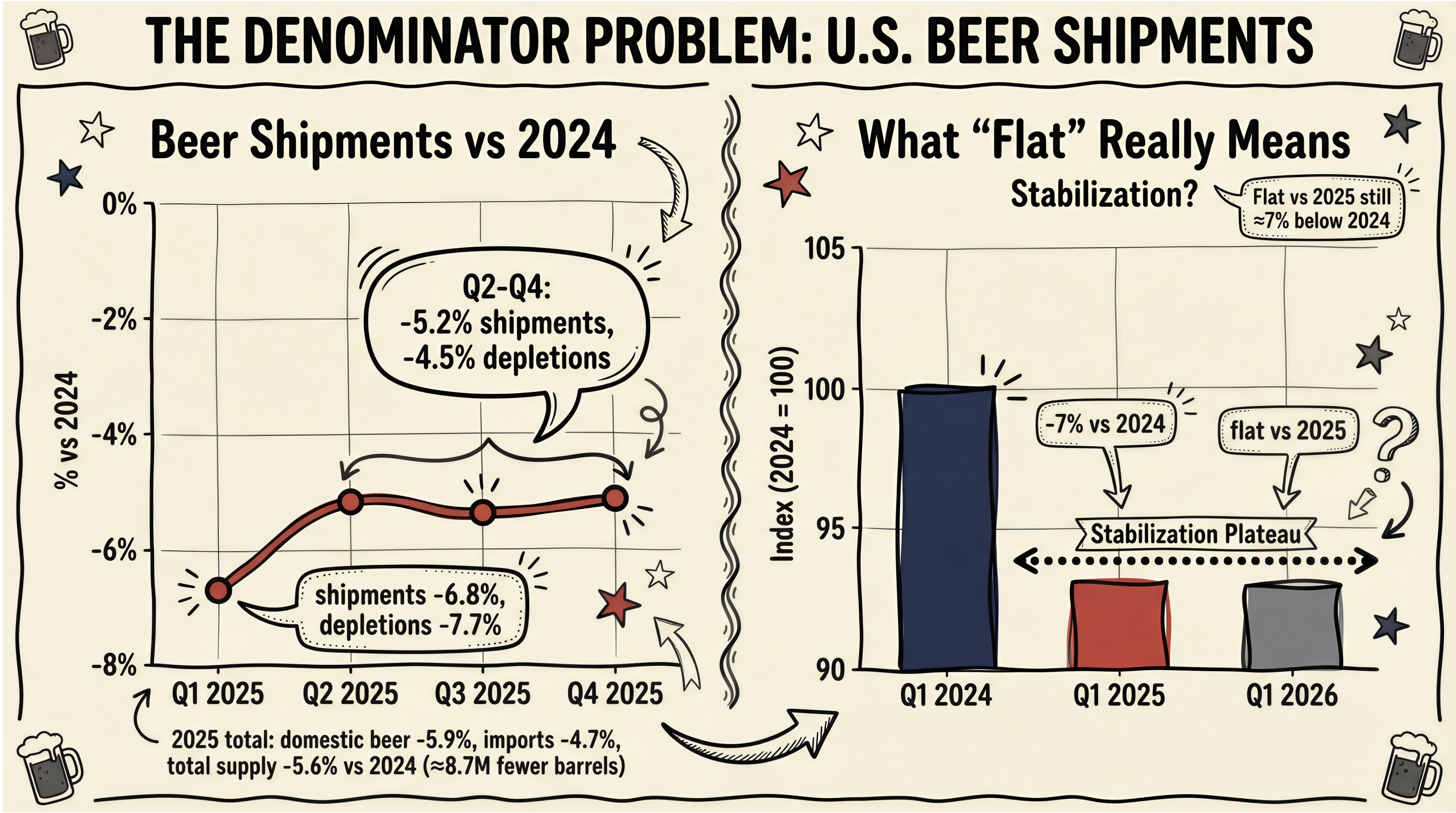

Beer Institute supply data for full-year 2025: domestic shipments down 5.9%. Imports down 4.7%. Total industry supply off 5.6%, roughly 8.7 million fewer barrels than 2024. Domestic shipments declined every single month.

But the decline wasn’t evenly distributed. As BI chief economist Andrew Heritage noted in his year-end supply commentary, Q1 marked “the steepest drop by far,” with shipments down 6.8% and depletions off 7.7% before moderating later in the year

Here’s what that means for 2026. When your comp is a quarter that fell nearly 7%, you don’t need a recovery to post growth. You just need to be less bad. If Q1 2026 comes in flat versus Q1 2025, that still represents a market sitting roughly 7% below 2024 levels. But the headline will read: “Industry stabilizes.”

This is denominator distortion. It will shape every growth headline for the next two quarters, so it’s worth naming clearly now.

When participation shrinks and frequency compresses, shipment math can improve without anyone actually drinking more often. A flat quarter today still represents millions of occasions that simply no longer exist. A Thursday that used to default to drinks is now a pickleball game, a DoorDash night, or an early bedtime. Those lost rituals don’t show up in headline growth rates, but do appear in the baseline.

The January Mirage

Those early January growth weeks felt good. Most prolonged consecutive growth in years, per Beer Institute commentary. Then the weather hit. Severe winter storms across major beer markets softened subsequent weeks.

The weather may well be the real explanation. But the pattern it creates is worth watching: early growth narrative followed by softening. Then comes an external variable that absorbs the blame. We’ve seen this sequence before. “Wait until spring.”

Meanwhile, according BI, the Super Bowl load-in data told its own story. Texas grew volume 2.6%. Every other state declined. Even during the single largest beer occasion of the year, national breadth was weak. Growth was geographically concentrated, not structurally distributed.

The K Continues to Shape

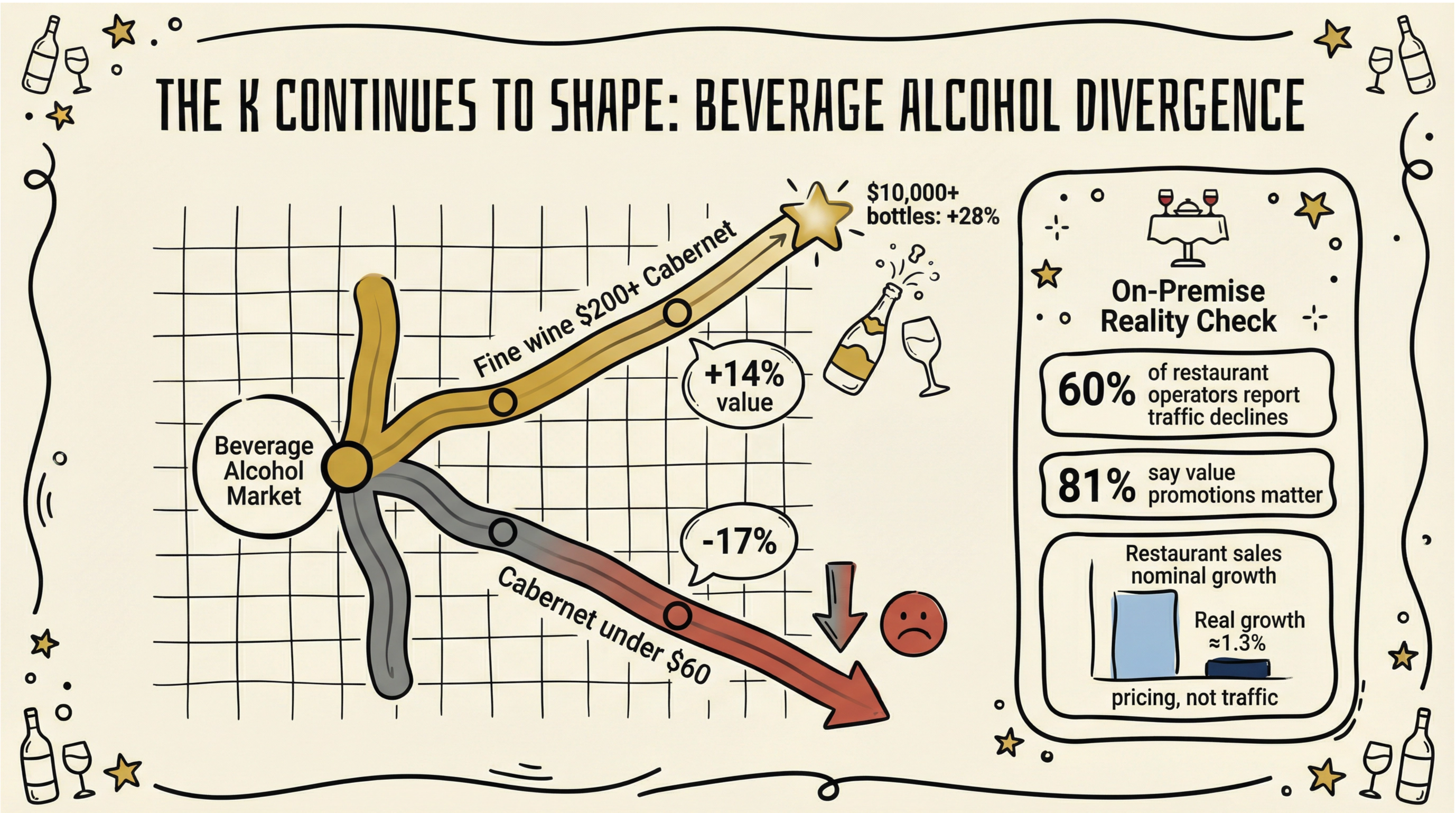

If you want to find growth in beverage alcohol right now, you can. You just have to know where to look and how narrow your perception needs to be.

Fine wine above $200 in Cabernet? Up 14% in value. Bottles north of $10,000? Up 28%. On-premise sweet spots in the $15-25 by-the-glass range and $75-150 bottle range? Holding firm. Luxury venues stable.

Now zoom out. Cabernet under $60? Down 17%. Sixty percent of restaurant operators reported traffic declines. The restaurant industry posted nominal sales growth, but real growth was a thin 1.3%.

This isn’t broad recovery. It’s concentrated resilience in income-segmented, channel-segmented, occasion-segmented pockets. Premium is carrying the system. That can be sustainable until it isn’t, but it’s a different story than the one “stabilization” implies.

The Actions Don’t Match the Words

If stabilization were structural, if executives actually believed it in their bones, you’d see expansion. Hiring. Innovation acceleration. Risk appetite.

Instead: Heineken is cutting 5,000-6,000 jobs, roughly 7% of its workforce. Treasury Wine suspended its dividend. Brown-Forman reversed inventory positions. Nineteen percent of Scottish distilleries face financial distress. Craft closures continue. SKU rationalization is accelerating across portfolios.

These are the behaviors of an industry protecting margin and preserving cash. Rational, yes. But capital posture is also a vote, and right now the votes are running against the narrative. If the outlook were broadly improving, you’d expect to see it in hiring decisions and innovation pipelines. So far, you don’t.

Event Density Is Not Frequency Recovery

The 2026 calendar is stacked. Super Bowl. World Cup. July 4th, which happens to be America’s 250th. NBA Finals. Stanley Cup. MLB All-Star. Compressed into roughly a six-week window.

Event density produces demand stacking, pull-forward purchasing, and temporary lift. It also produces the optical illusion of recovery. Shipment spikes during concentrated event windows look great in quarterly reports. They look less great when you realize they may be cannibalizing adjacent occasions rather than creating new ones.

This connects directly to the occasion framework I’ve been building all year.

Layer 1, the ambient habitual drinking that used to form the base of the system, continues to erode. Layer 3, the intentional high-stakes events, is concentrating rather than distributing. Fewer occasions producing larger spikes makes for volatile shipment patterns, and volatile patterns measured against weak comps produce the appearance of stabilization.

Layer 1 used to distribute volume across the calendar almost invisibly. No reason required. Just proximity, synchronization, and social permission. Layer 3 events are different. They need intention, planning, and a reason to show up. They concentrate energy rather than spreading it.

A system built on spikes is not the same system that once ran on repetition. When demand compresses into fewer, bigger moments, it can look healthy on the right weekend and hollow on an ordinary Wednesday. Whether that pattern reflects durable demand is a different question than what the quarterly report will say.

What “Stabilization” Actually Means

I’m not arguing that things aren’t improving. Declines are moderating. That’s real. What I’m suggesting is that the word “stabilization” is doing more work than the data can support.

The more useful question is whether the industry bruised or reconfigured. A bruise heals on its own. The pattern we’re seeing, lower ambient frequency, concentrated event demand, premium carrying the load, looks less like a recovery in progress and more like a system that found a new equilibrium at a lower level.

Which is also the tension sitting underneath Lewis’s reset comments. He’s right that Diageo has a mass market gap and right that premiumization alone isn’t enough. But the volume strategy he’s signaling assumes there’s share worth fighting for. That volume is just in the wrong segments, not permanently gone. If occasions are actually contracting, Sir Dave is competing harder for a bigger slice of a shrinking pie. Winning that fight likely still doesn’t solve the denominator.

Some of what drove that shift looks permanent. The midweek occasions that disappeared didn’t just soften, they got replaced. Wellness culture, cannabis destigmatization, the normalization of sober-curious identities, delivery apps that make staying in completely frictionless. These aren’t temporary headwinds waiting to reverse. They’re substitutes with real cultural momentum. A 28-year-old who organized their social life around group fitness and a Friday CBD drink isn’t a lapsed customer waiting to come back any time soon. They’ve built different rituals around different defaults, and those rituals tend to stick.

The optimistic counterargument is cohort-based: people have historically drunk more as they’ve aged into careers, families, and the social structures that come with them. That’s been true across generations. The question this cohort raises is whether the substitutes they have access to are more durable than the ones previous generations faced. It would be reasonable to guess that they are.

If stabilization is really a lower cultural equilibrium, fewer automatic occasions, more deliberate consumption, more price sensitivity, then the strategy isn’t to wait for the old frequency engine to restart. It’s to build for a world where drinking has to earn the occasion rather than assume it.

That changes what companies should do next. If you read the current moment as recovery, you protect legacy SKUs, slow portfolio pruning, delay channel resets, and underinvest in structural growth. If you read it as a new floor, you prune aggressively, rationalize distribution, focus on high-velocity formats, and rebuild occasion infrastructure from scratch.

One of those is a recovery strategy. The other is a redesign.

The Test

Structural recovery would look like broader geographic lift beyond single-state spikes: casual on-premise traffic coming back to something like a default, mid-tier price bands stabilizing, value promotion dependence easing. The distress headlines getting quieter.

It would also look like the return of low-friction social density. People saying yes to the extra round on a Tuesday. Bars seeing midweek rhythm again, not just weekend cliffs. Occasions that don’t need a marketing hook to exist.

Those signals aren’t here yet.

Maybe 2026 posts modest real volume growth. Maybe the event calendar provides enough lift to get there. Maybe Gen Z’s rising legal-age population finally converts to something durable. I genuinely hope so.

But hope doesn’t change what the data is saying. If 2026 looks better, the only question that matters is: what exactly improved?

If it’s the denominator, we haven’t stabilized. We’ve just stopped falling. And the difference between those two things is where the next five years of capital allocation gets decided.

Diageo knowing that answer is what Lewis was, in my opinion, really saying this week. When the company that spent a decade defining premiumization starts talking about price cuts and mass market gaps, the stabilization story deserves a harder look.